Read the latest issue of the Dairy Bar, a bi-weekly report from IDFA partner Blimling and Associates, Inc., a dairy research and consulting firm based in Madison, Wisconsin. The Dairy Bar features spotlight data, key policy updates, and a one-minute video that covers timely topics for the dairy industry.

Date of issue: June 24, 2020

[[trackingImage]]

[ Image ]

[ Image ]

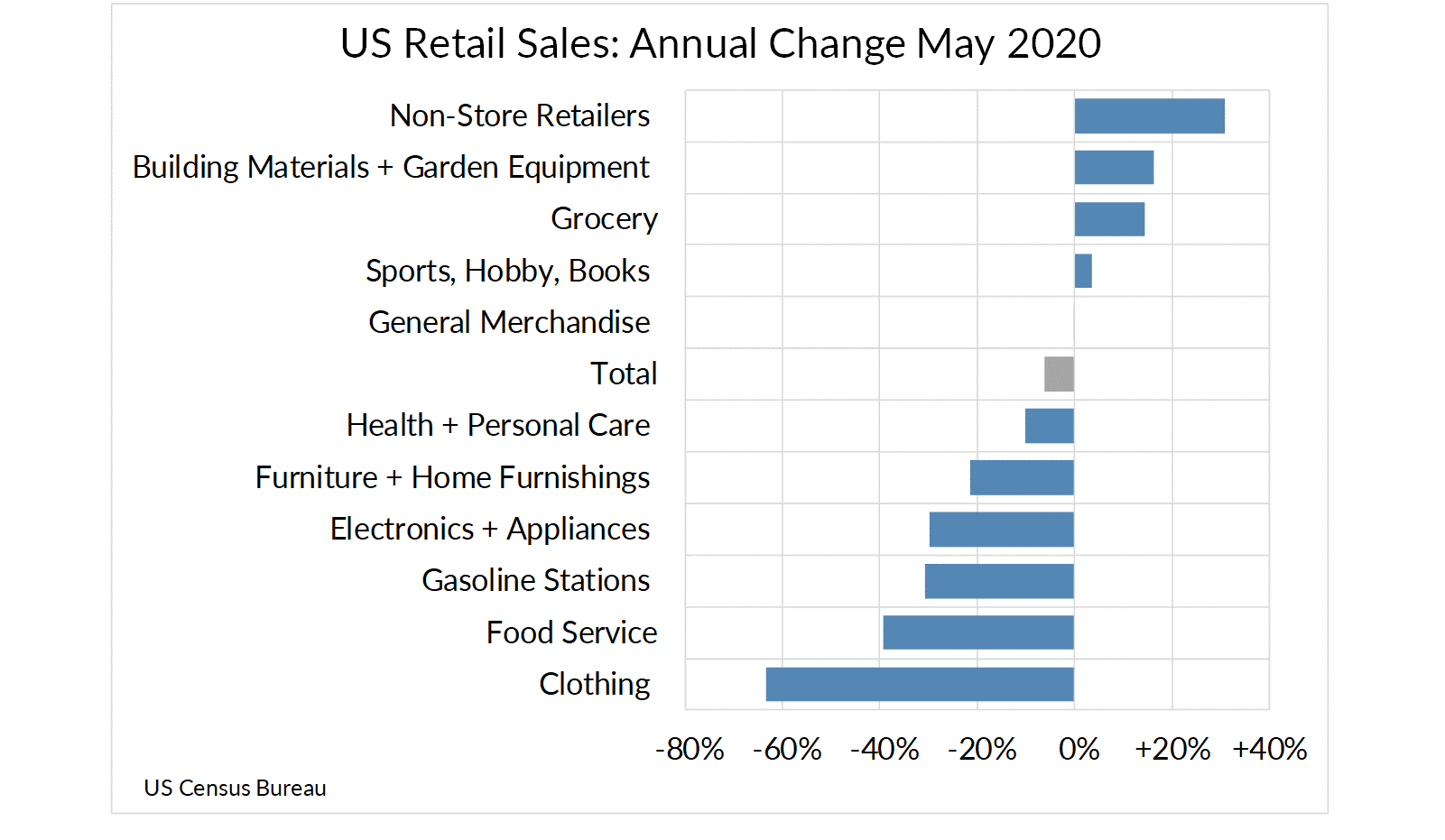

Quick Bites: Rebounding Retail Sales

In May, American consumers were not spending money on plane tickets or the latest fashion items. Instead, with stimulus checks in hand, consumers funneled dollars into online shopping, sporting goods, and sprucing up their backyards. Non-store retailers (aka e-commerce) saw a 31% bump in sales year-over-year to $86 billion. Building material and garden supply stores, meanwhile, saw a 16% boost. A quick look at Google Trends data shows a surge in searches for “Best Gas Grill 2020.” Pools are in high demand. With the pandemic still circulating, people seem keen on spending the summer at home, grilling up cheeseburgers and floating in the pool while waiting for their Amazon packages to get delivered.

Speaking of food, spending at grocery stores stayed strong in May. Food retailers took in nearly $73 billion, up about 15% from May 2019 and up 2% from April. Bars and restaurants continued to struggle, though, with sales totaling $39 billion, 39% less than 2019 but up 29% from April’s poor performance. June will likely feature continued rebounds in restaurant sales. Expect the data to keep skewing toward growth in grocery.

Today's Special

From +3% to -1% in the matter of three months. Since March, proactive steps by cooperatives and handlers to curb oversupply helped dairy producers rapidly respond to falling demand. In late April and into May, many handlers asked producers to trim output, and promised to offer penalties for milk produced beyond stated limits. Producers culled cows, adjusted milking schedules, and altered feed rations to meet the targets. Productivity took a major hit with milk output per cow falling 1.5% year-over-year, the largest contraction since 2001. Overall, May milk output decreased by 1% versus year-prior levels – the largest year-to-year decline since 2009. Production saw the biggest pull back in places with the most stringent cutback requirements like the Northeast, Southwest, and Midwest.

Fast forward to today and the demand situation is anything but dire, with cheese prices at all-time highs and Class III futures for the second half trading near $19 per hundredweight. If realized, that would be the highest second half since 2014. Plus, direct payments from USDA and Paycheck Protection Program dollars have eased the burden of low April milk checks. There’s plenty of cow power in the system today to quickly ramp production back up, with herd numbers still up 37,000 head from last May. At what point do producers start to add concentrates back to rations or change up the milking routine again? History says that it’s a relatively short road to recovery and the incentives are clearly there. But in many cases, supply restrictions are still in place. Some of those programs are set to run through July, while others are indefinite. Those programs could quell some producer growth appetites, though others may take the chance on oversupply penalties.

Something Sweet: The Cold Storage Minute

[IDFA Video Thumbnil] [[https://dairy.wistia.com/medias/dagl2auh4h]]