Read the latest issue of the Dairy Bar, a bi-weekly report from IDFA partner Blimling and Associates, Inc., a dairy research and consulting firm based in Madison, Wisconsin. The Dairy Bar features spotlight data, key policy updates, and a one-minute video that covers timely topics for the dairy industry.

Date of issue: May 27, 2020

[[trackingImage]]

[ Image ]

[ Image ]

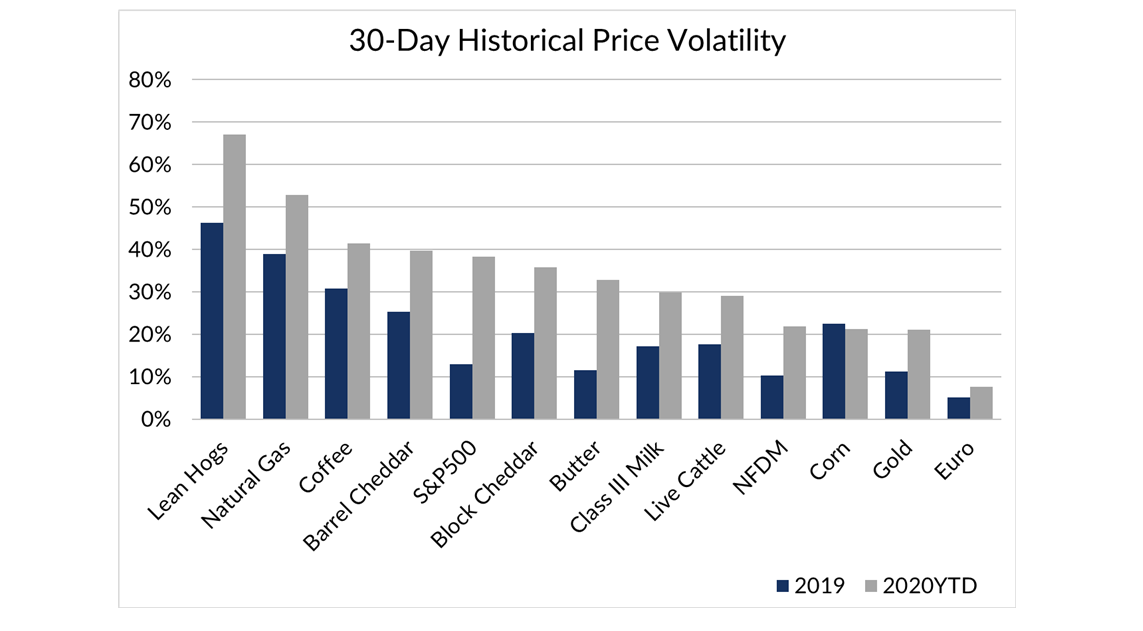

Quick Bites: Volatility in the Dairy Markets

Volatile. Very volatile. Dairy markets have been especially wild over the past several weeks. Take the block cheese market. It went from +$1.80 in mid-March to $1.00 in mid-April back to +$1.80 by mid-May. Phew. Enough to make you seasick.

The math bears out what you’ve been feeling. Year-to-date, 30-day historic price volatility in cheese and butter ranges between 30 and 40%. More volatile than corn. More volatile than the Euro. Equally as volatile as over the S&P 500 over the same period.

While the worst of the extreme movement may be in the rearview, few expect dairy markets to turn calm. Balancing and rebalancing demand between food service and retail will likely lead to further choppiness ahead.

Today's Special

Dairy demand has dominated conversations over the past several weeks with market participants trying to figure out which end is up. But supply has been equally mysterious. Too much supply yesterday, not enough today. What will tomorrow bring?

In late March, it seemed inevitable that there would be too much milk on the market for an extended period. Cooperatives and handlers, in response, asked producers to cut back supply where they could. And in many cases, they did just that. USDA’s latest Milk Production report showed April milk flows up 1.4% year-over-year, a slide from March’s +2.8%. And much of the reduction was done by cutting milk production per cow which fell from +2.2% year-over-year in March to +0.9% in April. Even still, there was too much. Spot milk in the Upper Midwest April was consistently trading at record low levels of around -$5 to -$7 under class. And milk that couldn’t find a home was getting dumped. Data from USDA suggests that more than 300 million pounds of milk may have been dumped in April – about 2% of U.S. milk supply for the month.

Fast forward to today. Spot milk in the Upper Midwest is trading at a premium to class in many cases and manufacturers are clamoring for more. Eight weeks ago, market participants wondered how quickly producers could turn output off. Today, the same people are wondering how quickly they can turn it back on. It seems likely that the rebound in milk flows could be fairly swift. Producers trimmed production by feeding and milking less. They did not aggressively cull cows. By the end of April, cow numbers – though down 4,000 head from March – were still 49,000 head above prior year levels. And with slaughter plants running with skeleton crews, animals have been slow to move out of the system through May. At the same time, June Class III milk futures prices are trading back above $17.50 per hundredweight and the second half of the year is trending above $16.00. Grain prices, meanwhile, have stayed weak. That’s creating incentive for dairy producers to get back into growth mode. Direct payments from USDA will help sweeten the pot, too, with payments expected to roll out in the coming weeks. Even with the improvement in the price outlook, growth in the second half may likely fall short of early 2020 expectations.

For more information on direct payments to producers, click here to read IDFA’s latest blog post.

Something Sweet: The USDA Minute

[IDFA Video Thumbnil] [[https://dairy.wistia.com/medias/dagl2auh4h]]